Update: Refer Payday Super content regarding Salary Sacrifice too, for specific treatments from 1 July 2026.

The reporting of salary sacrifice under STP2 has changed compared to STP1. From a processing perspective, salary sacrifice to super is unchanged. However, changes may be required to the manner in which some non-super salary sacrifice items, otherwise known as salary sacrifice other are processed.

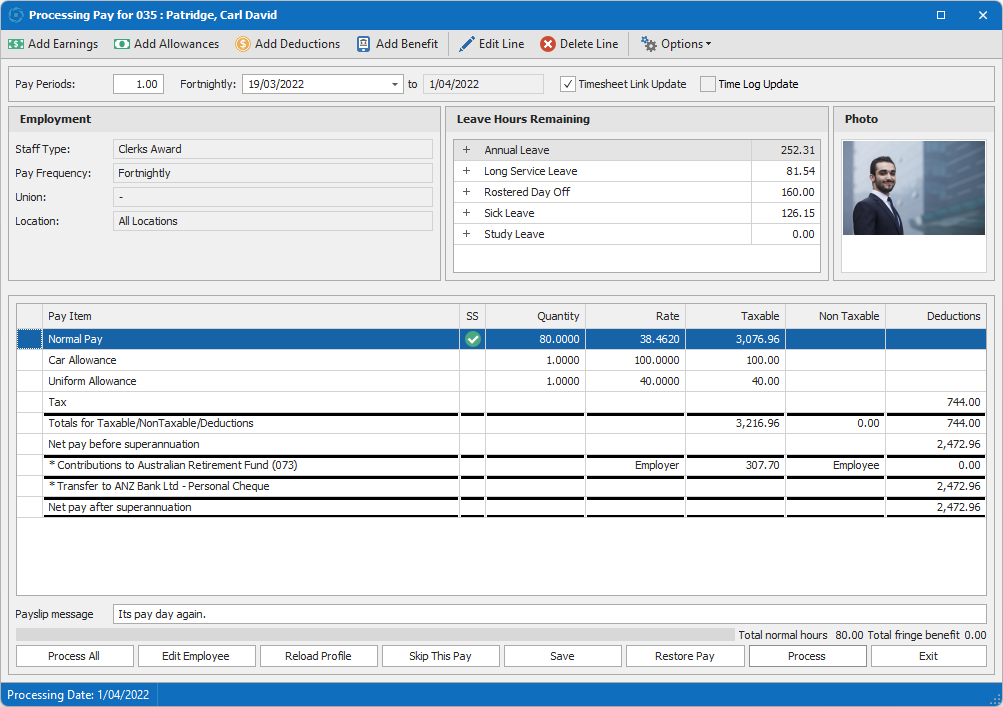

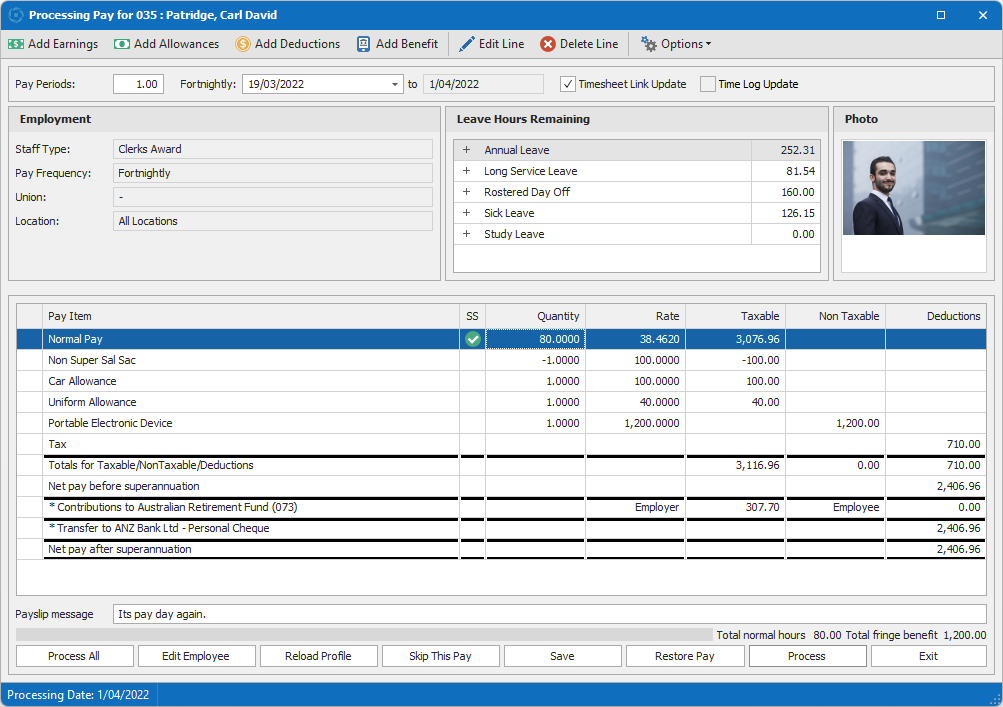

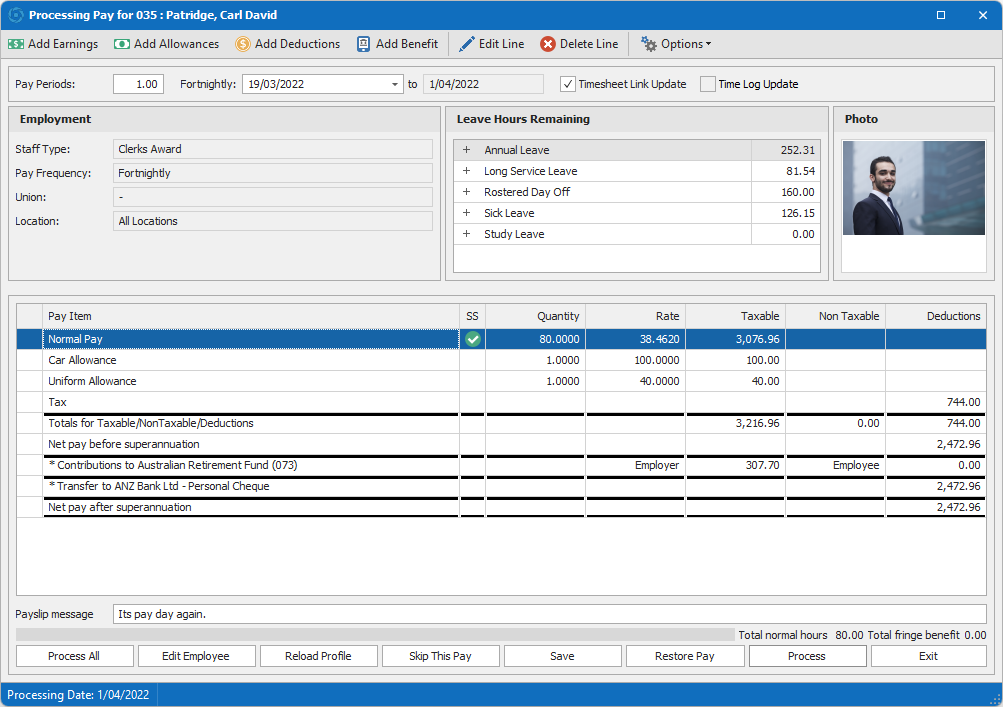

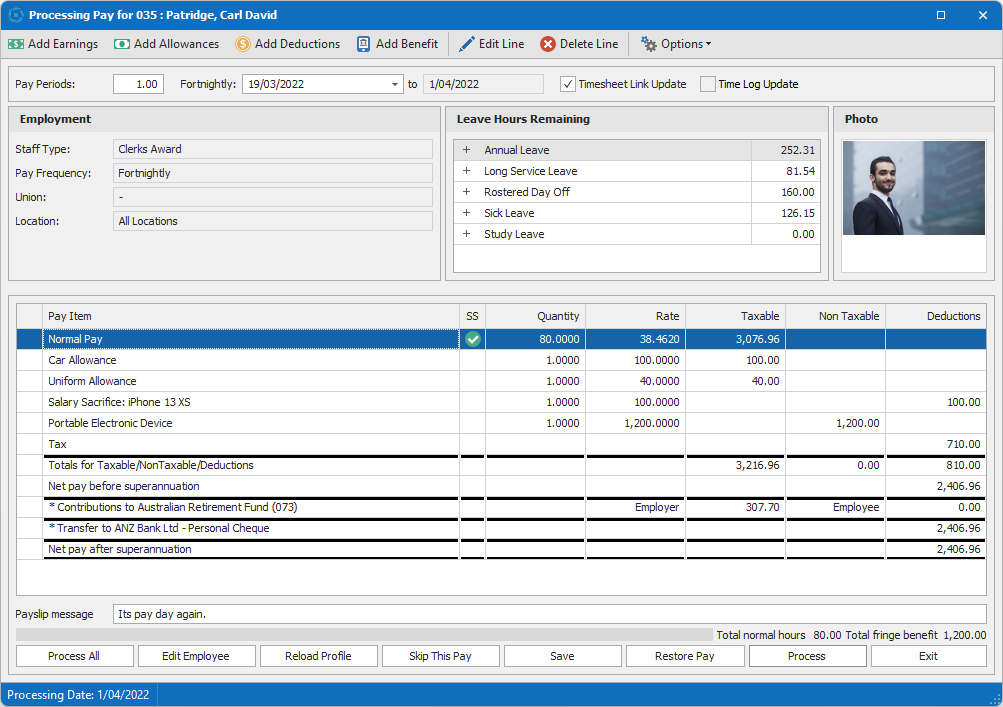

The concept of salary sacrifice reporting in STP2 is that the source of the salary sacrifice is grossed back up to its pre-sacrificed value and the salary sacrifice is reported separately.

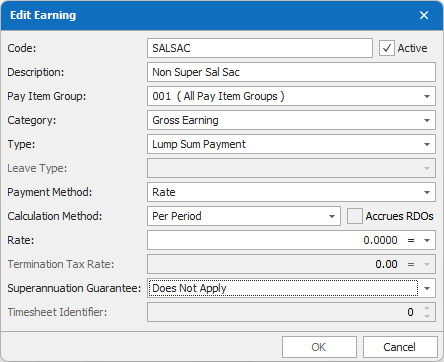

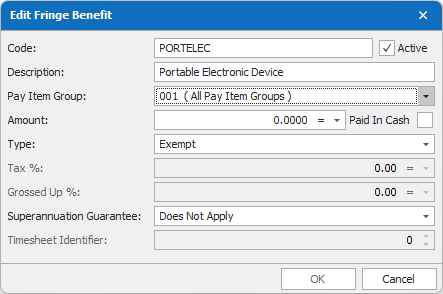

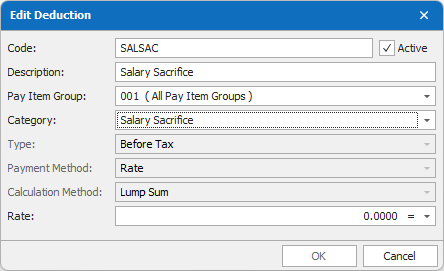

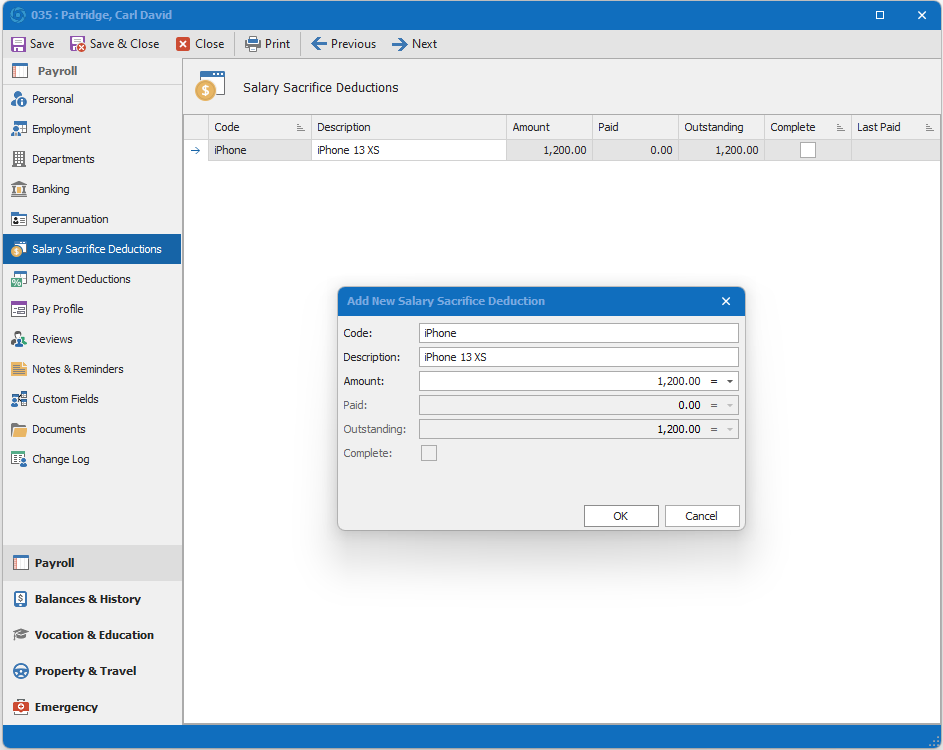

The key change that is required when processing salary sacrifice other for reporting under STP2 is that the sacrifice is now processed as deduction, rather than a negative earning item.

The following example looks at the pre-STP2 and post-STP2 methods of processing a salary sacrifice for an exempt benefit, such as a portable electronic device.